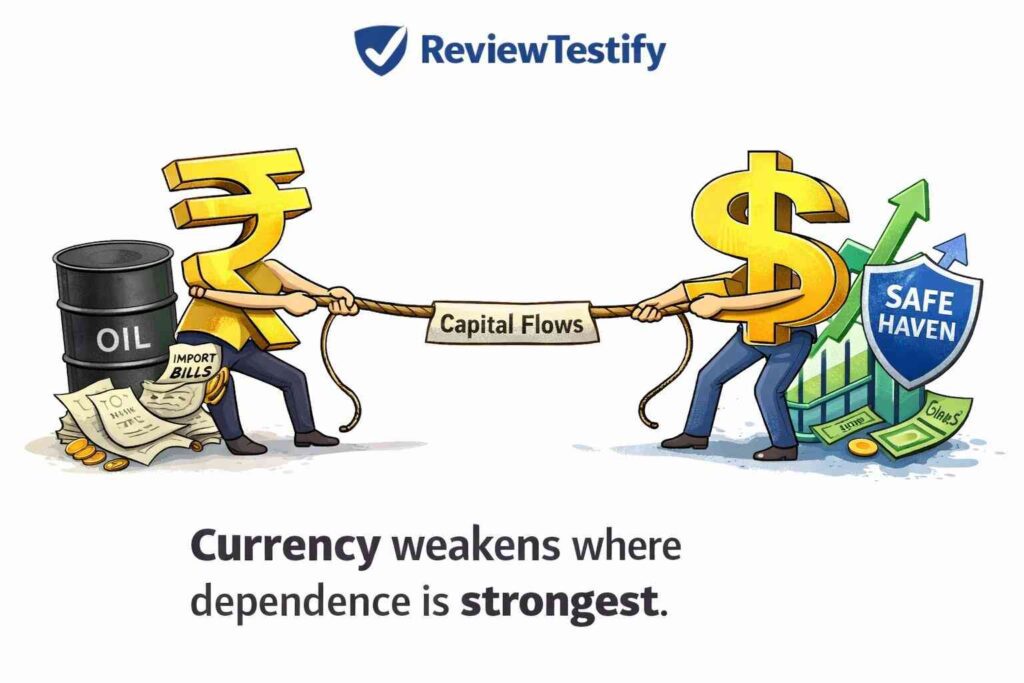

Rupee vs Dollar: INR Weak or the USD Strong?

Rupee vs Dollar: Is the INR Weak — or Is the USD Simply Dominating?

India’s economy is growing fast. GDP growth has stayed above 7% across multiple quarters in 2025. Inflation has cooled sharply, even flirting with deflation in food prices.

On paper, this looks like economic strength. Yet the rupee is hovering near historic lows against the US dollar.

This contradiction raises a real question:

Is the rupee weak — or is the dollar too strong?

Let’s break this down in this ‘hen or egg first’ article without noise.

Why a growing economy can still have a falling currency

Currency strength is not a trophy for GDP growth. It reflects capital flows, trade balance, interest rates, and global risk sentiment.

India’s growth is real. But so are its structural pressures:

- India imports far more than it exports.

- Oil, electronics, machinery, and gold are priced in USD.

- When the rupee falls, the import bill rises immediately.

Growth increases demand for imports.

If exports don’t grow at the same pace, the currency comes under pressure.

The RBI’s rate cuts: good for growth, bad for the rupee

With inflation falling below target, the RBI cut repo rates multiple times in 2025.

Lower rates:

✔ Encourage borrowing and spending

✘ Reduce returns on Indian bonds

Foreign investors compare yields globally. If US bonds offer better returns, money moves out of India.

When investors exit:

They sell rupees → buy dollars → INR weakens.

This is not a crisis. It’s basic capital flow math.

The global dollar effect: when the tide pulls everyone down

Even strong economies cannot escape a strong dollar.

The USD strengthens when:

- US bond yields are high

- Global uncertainty rises

- Investors seek safety

In such periods, all emerging market currencies weaken, regardless of domestic growth.

The dollar has a dual role:

- Investment currency

- Global safe haven

If the US slows and the Fed cuts rates, the dollar may weaken.

But if global fear rises, money still rushes into USD — pushing emerging currencies down.

India is caught in this crosscurrent.

India’s homegrown pressure points

Not all rupee weakness is external.

1. Trade deficit

India imports heavily, but exports grow slowly. This widens the deficit and weakens the currency.

2. Oil dependence

Crude oil is India’s biggest vulnerability.

A weaker rupee makes oil costlier — instantly raising national expenses.

3. FII behaviour

Foreign investors care about USD returns.

If they earn 10% in India but the rupee falls 3%, their real return is 7%.

Persistent rupee weakness triggers capital outflows, which further weaken the rupee.

This feedback loop is already visible in sustained FII selling.

What a weak rupee actually means for Indians

This isn’t abstract economics. It hits daily life.

Costlier essentials

- Fuel and transport

- Imported electronics

- Flights and international services

- App subscriptions priced in USD

Gold becomes expensive

Indians buy gold as a hedge — not just against inflation, but against currency depreciation.

Export benefits are limited

Only sectors with minimal import dependence — like IT services — benefit cleanly.

Manufacturing exporters often lose the advantage due to higher input costs.

The strange mix: high growth + low inflation

Near-zero inflation typically signals weak demand.

India, however, is seeing strong growth alongside falling food prices.

This suggests:

- Sector-specific price declines

- Strong services growth

- Statistical deflation, not economic weakness

In short: the economy is expanding, but the currency reflects structural gaps.

Final verdict: Weak rupee or strong dollar?

Both are true.

The dollar is strong due to global forces.

The rupee is pressured by structural realities:

- import dependence

- trade deficit

- capital outflows

This is not a verdict on India’s economy.

It’s a signal of where vulnerabilities still exist.

What matters next

The rupee’s path depends less on GDP headlines and more on structural shifts:

- Reducing oil dependence

- Boosting export competitiveness

- Deepening manufacturing

- Stabilizing capital flows

Until then, the rupee will remain sensitive to global tides — even when India grows faster than everyone else.

Research & Evidence Sources

- RBI & government trade data on deficits and imports

- USD/INR depreciation trends and record lows

- FII outflows and capital flight impact

- Strong dollar, oil dependence, global pressures